Travel Insurance

TRAVEL INSURANCE FAQ’S Why is travel insurance...

Read More

Financial Planning

Process & Benefits of Planning It’s important...

Read More

Trusts & Wills

Trusts Trusts TRUST APPLICATION Trust Administration Fee...

Read More

Medical Aid

Medical Aid Benefit Comparison Click here Helfin...

Read More

Short Term Insurance

Commercial Insurance Your house or buildings, vehicle,...

Read More

Tax Planning and Consulting

Services for the completion and submission of...

Read More

Long Term Assurance

Business Assurance We undertake a business assurance...

Read More

Group Benefits

In today’s highly competitive business environment, employers...

Read More

Retirement Benefits

South Africa’s Retirement Crisis March 2, 2021...

Read More

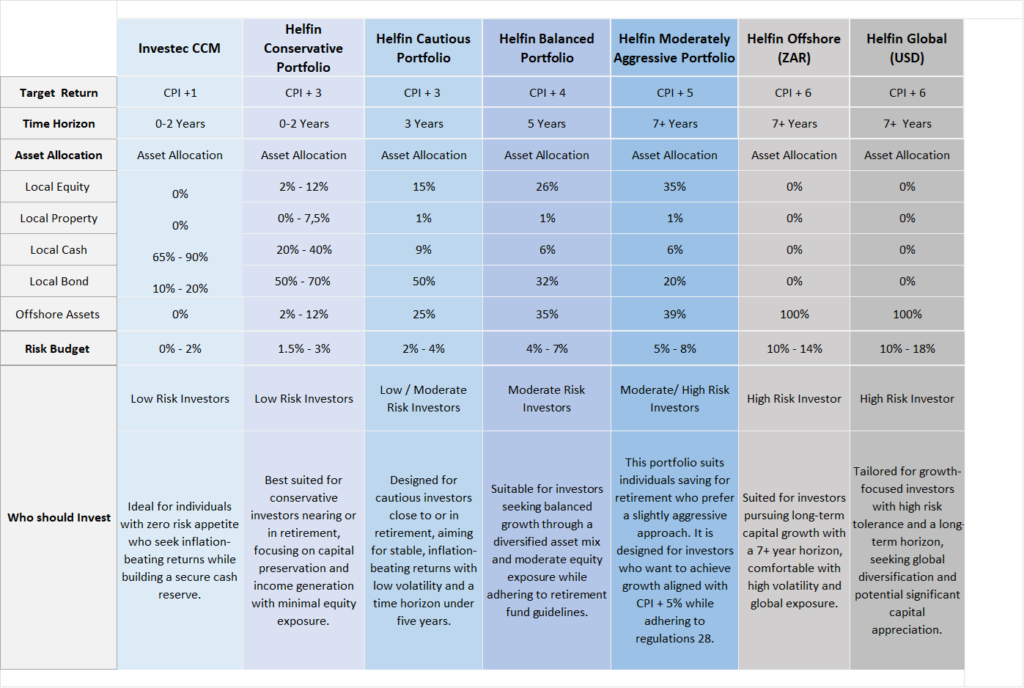

Local Investments

Helfin Private Wealth provides services on the...

Read More

International Investments

WHAT DO WE INVEST IN? We invest...

Read More