Revisiting Your Retirement

Essential Considerations for Those Who Previously Withdrew from Their Pension...

Read More

Changes to pensions in South Africa in 2023 – what you need to know

Changes to pensions in South Africa in 2023 – what...

Read More

Proposed retirement program amendments in South Africa

The National Treasury has published two papers on proposed retirement...

Read More

Please note that the below information is pending updates

Tax and retirement

Congratulations on your retirement. We believe that your retirement should be enjoyed and that you should not stress about tax. Therefore here are a few tips on the tax in respect of retirement.

Tax Treatment of lump sums paid by retirement funds

When you retire as a member of a pension fund, pension preservation fund or retirement annuity fund and you wish to take a portion of your retirement interest as a lump sum, you are allowed to take (commute) a lump sum equal to a maximum of one-third of the retirement interest in that fund, unless the entire value of the fund does not exceed R247 500 in which case you may take the full retirement interest as a lump sum.

When you retire and you are a member of a provident fund or provident preservation fund, your retirement interest is usually paid by way of a lump sum unless the rules of such a fund provide for the payment of an annuity on a member’s retirement.

If you are already retired and in receipt of annuity income from a living annuity arrangement, you are allowed to commute the amount as a lump sum, if at any time the full remaining value of the assets becomes less than R50 000.

Tax will be calculated on the gross retirement fund lump sum benefit after having taken into account, for example, contributions to a retirement fund which did not previously rank for deduction or which were not exempted from normal tax.

Basically what this means is that an individual is entitled to claim a deduction of contributions made to certain retirement funds. However, these contributions, for tax purposes, are subject to limitation. If the deduction is limited, the amounts are carried forward to the following year of assessment and are compounded. When the individual retires, for example, the compounded or excess contributions that did not previously rank for deduction or which were not exempted, can be used to reduce the gross lump sum figure on which the tax will be calculated, This will be illustrated by way of an example below.

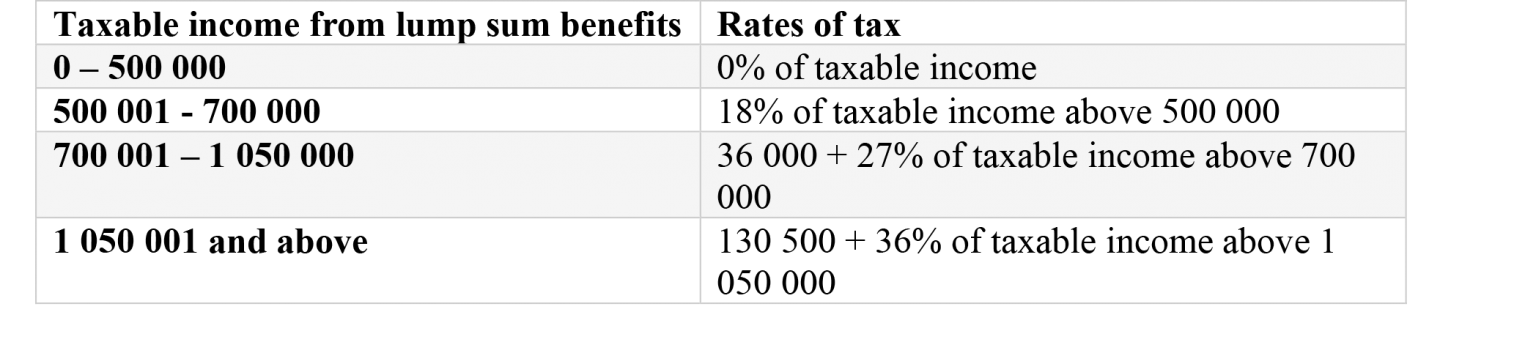

The lump sum is taxed upon retirement using special tax rates, as indicated below:

Example

X received a lump sum of R682 000 from the ABC Pension Fund, and had received no previous lumps sums prior to this. Over many years, the total contributions which did not previously rank for deduction or qualify for exemption in X’s hands amounted to R50 000. Calculate the normal tax payable on this lump sum.

Result

The gross lump sum on which normal tax will be calculated amounts to R682 000 less R50 000, which equals R632 000. R632 000 falls within the taxable income bracket of R500 001 to R700 000. The normal tax is therefore 18% of the taxable income above R500 000. Thus:

Normal Tax

= 18% of (R632 000 – R500 000)

= 18% of R132 000

= R23 760

The normal tax on the lump sum of R682 000 therefore amounts to R23 760, and the net lump sum after tax (“cash in pocket”) would equal R658 240.

It is important to note that ALL lump sums received from a retirement fund, whether as a result of retirement or not (and from an employer in respect of a severance benefit) are taxed on a cumulative basis. The significant impact of this is that, when the member eventually retires, the total value of all the lump sum benefits received by the member after 1 October 2007, will be taken into account when calculating the tax payable on the member’s current retirement fund lump sum benefit.

Tax treatment of annuity income

As indicated above, the two thirds of the retirement interest in respect of pension, pension preservation or retirement annuity is received in the form of an annuity (regular pension). If the income from your annuity exceeds the tax threshold, tax is payable on the amount. The tax thresholds are as follows:

- For the 1 March 2021 to 28 February 2022 year of assessment for the tax season starting during 2022:

- Person below the age of 65 – R87 300 per annum

- Person aged 65 and above but not yet 75 – R135 150

- Person aged 75 and above – R151 100.

- For the 1 March 2020 to 28 February 2021 year of assessment for the tax season starting during 2021:

- Person below the age of 65 – R83 100 per annum

- Person aged 65 and above but not yet 75 – R128 650

- Person aged 75 and above – R143 850.

- For the 1 March 2019 to 29 February 2020 year of assessment for the tax season starting during 2020:

- Person below 65 – R79 000 per annum

- Person 65 and above but not yet 75 – R122 300

- Person 75 and above – R136 750.

- For the 1 March 2018 to 28 February 2019 year of assessment for the tax season starting during 2019:

- Person below 65 – R78 150 per annum

- Person 65 and above but not yet 75 – R121 000

- Person 75 and above – R135 300.

- For the 1 March 2017 to 28 February 2018 year of assessment for the tax season starting during 2018:

- Person below 65 – R75 750 per annum

- Person 65 and above but not yet 75 – R117 300

- Person 75 and above – R131 150.

- For the 1 March 2016 to 28 February 2017 year of assessment for the tax season starting 1 July 2017:

- Person below 65 – R75 000 per annum

- Person 65 and above but not yet 75 – R116 150

- Person 75 and above – R129 850.

- For the 1 March 2015 to 29 February 2016 year of assessment for the tax season that started 1 July 2016:

- Person below 65 – R73 650 per annum

- Person 65 and above but not yet 75 – R114 800

- Person 75 and above – R128 500

It is important to note that, taking the above factors into account, even if you are no longer working, but are in receipt of annuity income, you might still continue paying tax. Each year you will have to declare your income from your annuity and any other income (e.g. investments income) you may have on your tax return (ITR12).

Above information sourced from SARS