Essential Considerations for Those Who Previously Withdrew from Their Pension

Question:

I have recently quit my job to join a different company. Now, I wish to withdraw my pension funds, but I’ve been informed that it may not be possible if I have already taken out all my pension in 2014. Can you please verify this information for me?

Response: 1

Upon resigning, individuals are typically permitted to access their entire provident and pension funds. However, it is important to note that this approach is not advisable due to heavy taxation and the depletion of retirement savings intended for the future. It is recommended to consider alternative options that preserve your retirement funds.

Regarding your inquiry, the withdrawal of your pension will indeed be permitted. However, it’s important to note that you may have already exhausted your tax-free benefit for such withdrawals, which is typically a one-time opportunity. When making the withdrawal, a sliding scale will be applied to the total sum of previous lump sums withdrawn along with the current withdrawal. The initial amount of R27,500 (increased from R25,000 in the 2023 budget speech) will remain tax-free, while any additional amount will be subject to a progressive tax rate based on the sliding scale.

At present, if you have already utilized the tax-free benefit, your withdrawal will be subject to full taxation.

It is crucial to comprehend the consequences of withdrawing your retirement funds before reaching retirement age and to consider how it aligns with your future plans. It is highly recommended to reinvest your retirement savings either within your new company or personally when transitioning between employers. By doing so, you can avoid sacrificing a significant portion of your savings to the South African Revenue Service (SARS) and also prevent the loss of valuable time in the market.

By continually restarting your financial journey, you are placing undue and unrealistic financial pressure on yourself, particularly in terms of catching up to secure a comfortable retirement.

One common recommendation we frequently discuss is the need to invest approximately 15% of your income over a 40-year working period to achieve a replacement ratio similar to your pre-retirement income. This estimate takes into account a 6% inflation rate and an average return of 10% throughout that duration. However, it’s important to note that the 15% rule can vary over time. For instance, if you begin investing in your 40s or 50s, the percentage required would be significantly higher.

Dipping into your savings and starting over each time will not only alter the desired outcome but also increase the level of contribution needed to ensure a comfortable retirement. Regrettably, only 6% of South Africans are currently able to retire comfortably, with an average replacement ratio of 31% (as reported by FAnews and AlexForbes). It is doubtful that the average individual would be able to sustain a comfortable lifestyle with just 31% of their previous income.

This emphasizes the significance of recognizing the value of preservation, regardless of the initial amount involved. The advantages of compound interest and allowing time to work in the market become immensely valuable over the long term.

The following example demonstrates the power of preservation:

Response: 2

Despite having withdrawn your pension in 2014, you still have the option to make a withdrawal from your pension fund. Here are the available options for you to consider.

Upon resigning from a company, individuals have several options to choose from. The first option is to receive the accumulated benefit as a single cash lump sum. The second option involves transferring the funds from their pension fund into a preservation fund. The third option allows for a combination of the two, wherein a portion of the capital is withdrawn as a lump sum while the remaining balance is transferred to a preservation fund.

Alternative 1

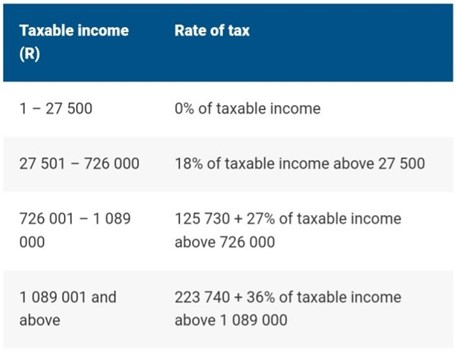

This decision is especially important for individuals who require immediate access to funds for emergency purposes. If you decide to receive the benefit as a lump-sum cash payment, it is essential to be aware that taxation will be applied based on the withdrawal tax tables (see tables below). It’s important to note that since you have already made a withdrawal from a retirement fund previously, the tax exemption of R27,500 does not apply in this case.

Alternative 2

A preservation fund serves as an investment tool specifically created to assist individuals in preserving and safeguarding their retirement savings upon resigning from their employment. Once the funds have been transferred to a preservation fund, the standard retirement regulations come into effect. This implies that when you reach retirement age, you have the choice to withdraw one-third of the accumulated amount as a cash lump sum, while the remaining two-thirds can be invested in a compulsory life or living annuity.

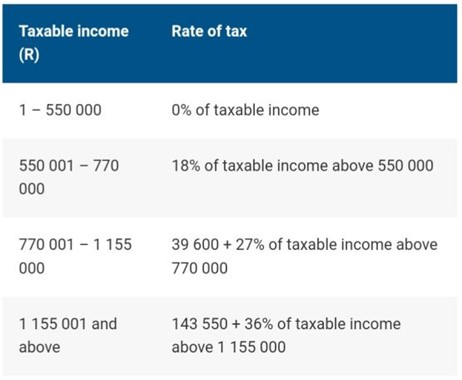

If you have made withdrawals from any retirement fund, whether it’s a pension, provident fund, or retirement annuity, before or after retirement, it will decrease the tax-free portion accessible to you. It is crucial to understand that the tax-free portion of R550,000 is an accumulated total for your entire lifetime.

If you possess multiple retirement funds and you decide to retire from one of them, utilizing your entire tax-free portion, it is important to note that when you retire from another fund in the future, you will be subject to taxation on the full cash lump sum benefit without any remaining tax-free allowance.

Additionally, when your funds are invested in a preservation fund, you have the option for a one-time full or partial withdrawal before reaching retirement age (55 years). However, once this withdrawal is made, you will not be able to make any further withdrawals until you reach the designated retirement age. It is important to be aware that this withdrawal will be subject to taxation in accordance with the withdrawal tax tables provided below.

Alternative 3

This option is suitable for investors who wish to preserve their retirement funds while needing access to a portion of their capital for emergencies. One possibility is to withdraw a specific portion of your capital as a lump sum while transferring the remaining balance to a preservation fund. However, it is crucial to acknowledge that this approach incurs additional costs, as it involves being subject to taxation twice.

Rules at retirement

Provident fund

Contributions made prior to 1 March 2021 are referred to as the “vested” portion of your provident fund and are exempt from the two-thirds annuitization rule. When current members of the provident fund reach retirement, they will retain the option to receive the complete accumulated value of the vested portion of their investment as a single payment, similar to the original allowance they had.

Pension fund

In the case of a pension fund, there is no concept of a vested portion. This implies that all contributions made to the pension fund will be subject to the two-thirds annuitization rule. Under this rule, you will have the option to withdraw one-third of the accumulated amount as a cash lump sum, while the remaining two-thirds must be invested in a compulsory life or living annuity.

Although the temptation to withdraw funds from your retirement account when changing jobs may arise, the scenario alters when the funds are needed for emergencies. It is consistently recommended to prioritize saving for retirement, with the objective of attaining a comfortable lifestyle during the post-employment years.

If you have not yet retired, our recommendation is to preserve your funds to enable them to continue growing.

Retirement tax table

Withdrawal tax table

This article has been reproduced by courtesy of Moneyweb.

Please note that any information in our posts, documents, infographics, emails etc is general information and should not be considered as providing financial advice. We therefore disclaim all liability and responsibility arising from any reliance placed on such information by any reader, client or visitor to our website. Though we make every effort to ensure the accuracy of the information provided we accept no liability for any inaccuracies.